We use cookies on our website to analyze website usage and to help secure the website against misuse.

Advertising and functional cookies are not used in our site or our web application products.

By clicking “Accept Essential Cookies Only”, you consent to us placing these cookies.

Learn how to apply accounting rules to different types of asset for IFRS, IAS, GAAP and Tax Depreciation

How to Depreciate Property and Assets in the UK

Overview

Depreciation allocates the cost of an asset over its useful life. Instead of taking the entire cost of the asset as a loss at the point of purchase,

deprecation allows you to spread the cost over several years. This results in higher profit in the year of purchase, but also higher corporation tax.

In the UK, depreciation is not recognised for tax purposes,

but is used for financial reporting under standards such as FRS 102 and IFRS. For tax purposes, we use Capital Allowances, which are explained below.

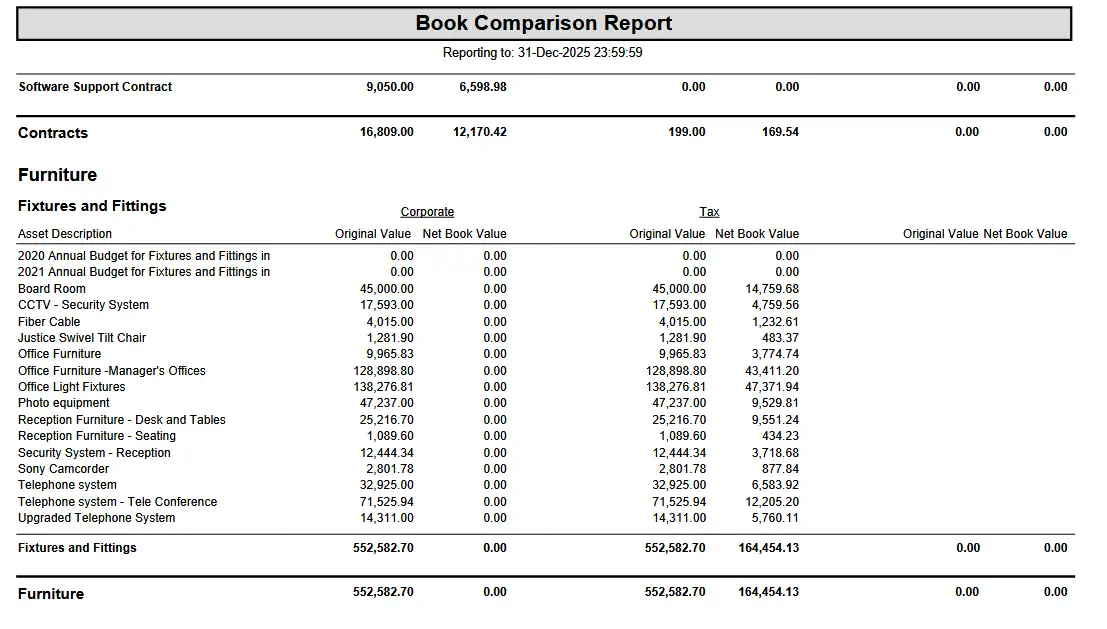

Typically UK businesses will calculate depreciation for financial reporting, and calculate Capital Allowances in a separate accounting book.

The relevant frameworks are:

FRS 102/UK GAAP applies depreciation based on useful life and residual value

IFRS/IAS 16 allows systematic depreciation, with useful life and residual value reviewed annually

Tax Depreciation is not used, instead capital allowances apply

Capital Allowances

Capital allowances allow businesses to deduct the cost of capital assets, including IT equipment, from their taxable profits.

This applies when purchasing, using, and disposing of assets.

When an asset is sold or scrapped, a balancing charge or allowance may apply to adjust the total relief claimed.

A balancing charge increases taxable profits if an asset is sold for more than its tax written-down value, while a balancing allowance provides relief if sold for less

There are three types of capital allowances relevant to IT assets:

The Annual Investment Allowance (AIA) gives 100% relief on qualifying assets in the year of purchase, up to a specified limit

Writing Down Allowance (WDA) is used when assets don't qualify for AIA or when AIA limits are exceeded. Applies a fixed percentage of the remaining value each year

Balancing Allowances and Charges apply adjustments when an asset is disposed of for more or less than its net book value

A business purchasing £50,000 in IT equipment can claim the full amount under AIA, reducing taxable profits in the year of purchase.

From 2019 to 2025 the annual AIA limit was £1,000,000 for qualifying expenditure.

xAssets Fixed Asset Management Software tracks asset acquisition cost,

depreciation, and disposal value, providing the reports and data needed to calculate capital allowances and these can be

calculated for you into a separate accounting book, and can be viewed alongside corporate and GAAP reporting.

If you spend more than £1m on Capital Assets in one financial year, you can still claim allowances, but not under the AIA.

For these assets you claim a writing down allowance. Some assets

qualify for 100% writing down, others for 50% under a first year allowance.

The following documents help to understand capital allowances:

Within the xAssets solution, depreciation rules operate default values at the Category level, and are assigned

to individual assets when the assets are created. You can edit the default or deploy specific rules to specific assets, but for most

customers it is sufficient to allow the rules to apply at Category level.

For example, a £10,000 server with a 5-year life would depreciate £2,000 annually under straight-line.

Depreciation Methods

Straight-Line: Equal charge each year:

Annual Depreciation = (Cost – Residual Value) / Useful Life

Reducing Balance: Fixed percentage applied to net book value:

Depreciation = Opening NBV × Rate

Units of Production: Based on usage rather than time. The xAssets software can calculate depreciation for

this rule with an API connection or a feed from any units of production data source.

The xAssets Depreciation Toolset includes the ability to create any depreciation formulae. Common depreciation scenarios such as

Straight line, Declining Balance, SYD, Units of Production, GDS, MACRS and ACRS (US only), Mid Month, Half Year, Mid Quarter, are all supported "out of the box",

and more formulae can be added if needed.

Components

With IFRS, parts of an asset with different recovery periods (different useful lives) are depreciated separately. E.g. A building may be split into structure, air conditioning,

and lifts all depreciated separately.

In real terms you simply store these as separate asset records with inter-asset relationships

and each one carries the value to be depreciated for that component.

Revaluation and Impairment

Revaluation: Optional under IFRS; assets can be revalued to fair value

Impairment: Required if carrying value exceeds recoverable amount

Asset Disposal

When an asset is disposed, we write off its remaining net book value, but we add or subtract the balances if the asset was sold and if there was a cost of sale.

Capital Allowances are calculated in a separate accounting book

Componentisation and revaluation tracking

Custom depreciation profiles

Automated monthly journals

Full audit trail of changes

Construction in Progress

This enables compliance with financial reporting and audit requirements for organisations with 200 to 100,000 assets.

Summary

Depreciation under UK accounting rules requires application of depreciation rules based on asset categories and standards.

For compliance and audit readiness, fixed asset software solutions such as xAssets Fixed Asset Management Software

ensure accuracy, transparency, tax compliance, and alignment with standards.

Get a Demo

What’s Included?

Demo shaped to your needs

Free instance

Free Instances Explained

Free instances are free forever and can show demo data or your data.

IT asset management free instances

Single user, 100 endpoints, 1,000 total assets

Includes network discovery (optional)

SNMP based devices are included free

Single Sign On (SSO)

Does not support Intune, SCCM, procurement, contracts, barcoding, configuration, or workflow

Fixed asset management free instances

Single user, 1,000 fixed assets

Includes all fixed asset register features

Single Sign On (SSO)

Does not support depreciation, CIP, procurement, barcoding, planned maintenance, configuration, or workflow